A standard piece of advice to researchers in math-oriented fields aiming to publish a popular book is that every equation reduces the readership by a factor of x (x can range from 2 to 10, depending on who is giving the advice). Thomas Piketty’s Capital has only one equation (or more precisely, inequality), at least only one that anyone notices, but it’s a very important one. Piketty claims that the share of capital owners in national income will tend to rise when the rate of interest r exceeds the rate of growth g. He suggests that this is the normal state, and that the situation prevailing for much of the 20th century, when r was less than g, was an aberration.

I’ve seen lots of discussion of this, much of it confused and/or confusing. So, I want to offer a very simple explanation of Piketty’s point. I’m aware that this may seem glaringly obvious to some readers, and remain opaque to others, but I hope there is a group in between who will benefit.

Suppose that you are a debtor, facing an interest rate r, and that your income grows at a rate g. Initially, think about the case when r=g. For concreteness, suppose you initially owe $400, your annual income is $100 and r=g is 5 per cent. So, your debt to income ratio is 4. Now suppose that your consumption expenditure (that is, expenditure excluding interest and principal repayments) is exactly equal to your income, so you don’t repay any principal and the debt compounds. Then, at the end of the year, you owe $420 (the initial debt + interest) and your income has risen to $105. The debt/income ratio is still 4. It’s easy to see that this will work regardless of the numerical values, provided r=g. To sum it up in words: when the growth rate and the interest rate are equal, and income equals consumption expenditure, the ratio of debt to income will remain stable.

On the other hand, if r>g, the ratio of debt to income can only be kept stable if you consume less than you earn. And conversely if r < g (for example in a situation of unanticipated inflation or booming growth), the debt-income ratio falls automatically provided you don’t consume in excess of your income.

Now think of an economy divided into two groups: capital owners and everyone else (both wage-earners and governments). The debt owed by everyone else is the wealth of the capital owners. If r>g, and if capital owners provide the net savings to allow everyone else to balance income and consumption, then the ratio of the capital stock to (non-capital) income must rise. My reading of Piketty is that, as we shift from the C20 situation of r ≤ g to one in which r>g the ratio of capital to stock to non-capital income is likely to rise form 4 (the value that used to be considered as one of the constants of 20th century economics) to 6 (the value he estimates for the 19th century)

This in turn means that the ratio of capital income to non-capital income must rise, both because the capital stock is getting bigger in relative terms and because the rate of return, r, has increased as we move from r=g to r>g. For example if the capital-income ratio goes from 4 to 6 and r goes from 2 to 5, then capital incomes goes from 8 per cent of non-capital income to 30 per cent[^1]. This can only stop if the stock of physical capital becomes so large as to bring r and g back into line (there’s a big dispute about whether and how this will happen, which I’ll leave for another time), or if non-capital owners begin to consume below their income.

There’s a lot more to Piketty than this, and a lot more to argue about, but I hope this is helpful to at least some readers.

[^1]: Around 20 per cent of GDP is depreciation, indirect taxes and other things that don’t figure in a labor-capital split, so this translates into a fall in the labor share of all income from a bit over 70 per cent to around 50 per cent, which looks like happening.

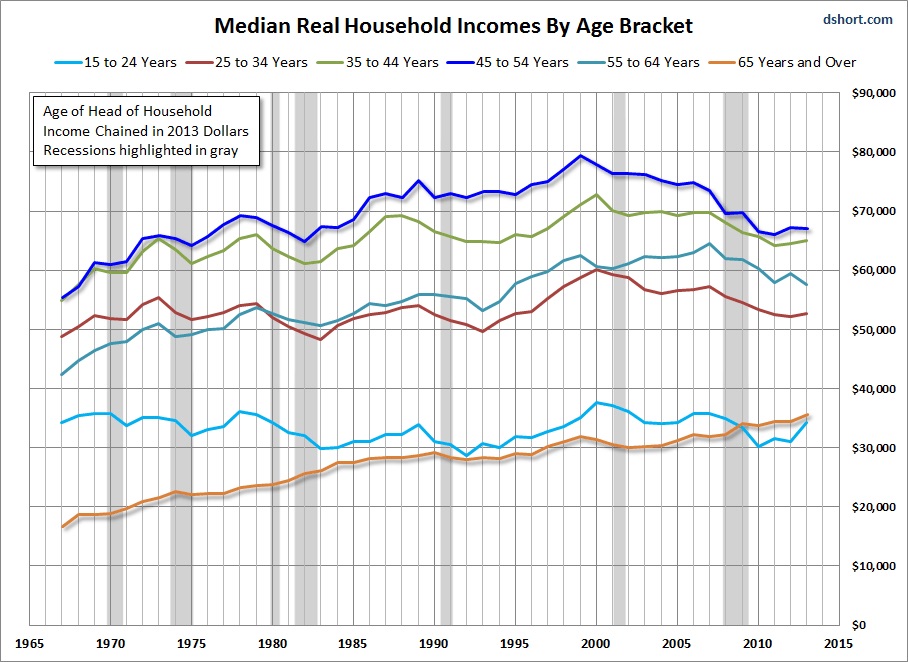

As can be seen, the group suffering the biggest loss, relative to older cohorts at the same age, are those households with heads aged 45-54 in 2013, a mix of late Boomers (for aficianados, this group is called Generation Jones) and early X-ers. But the main point is that median household income is falling for all groups except the 65+ cohort (mostly called Silents in the generation game). Part of this is due to declining household size, but (IIRC) household size has stabilized recently as forming a new household has become less affordable.

As can be seen, the group suffering the biggest loss, relative to older cohorts at the same age, are those households with heads aged 45-54 in 2013, a mix of late Boomers (for aficianados, this group is called Generation Jones) and early X-ers. But the main point is that median household income is falling for all groups except the 65+ cohort (mostly called Silents in the generation game). Part of this is due to declining household size, but (IIRC) household size has stabilized recently as forming a new household has become less affordable.