Here’s bit of bad news for my American Democrat friends; your candidate is dying on his arse in the Iowa Electronic Markets at the moment.

Here’s another bit of bad news; even at these prices, he’s still overvalued.

Note to readers. There is quite a lot of financial jargon in this post, because I’m dealing with quite a few issues that are only of interest to finance bods (and only marginally to them). The interesting stuff is toward the end.

I mean “Overvalued” in a technical sense here; given the prices of the other contracts trading on IEM, the “DEM04” contract on the winner-takes-all market should be priced significantly lower than the 0.454 which was its price as of the last trade when I was writing this.

I found out this little anomaly earlier this year, when I was playing around with get rich quick schemes[1] and idly wondering whether I could put together a program-trading system that would dump large numbers of trades onto the IEM all at once and make a few of my enemies shit their pants. I assumed it was due to teething troubles as the market for the ’04 Presidential race settled down, and that things would regularise soon enough.

The issue was, that I was working on some Visual Basic code to try and calculate the “implied volatility”[2] of the vote-share market from the WTA market in order to compare it against the realised volatility. I’ve worked a bit with the Black-Scholes model for pricing binary options in the past, and I know that the sensitivity to volatility of this kind of option is a pretty badly-behaved function, so it didn’t surprise me that the implied volatility formula I’d ripped off from Paul Wilmott‘s book didn’t seem to work. What did surprise me is that when I’d changed the code around, put in a more robust optimisation routine, corrected a few of my arithmetic errors and debugged, it still didn’t work. I was buggering around with this, off and on, for about two months, and nothing I could do could get it to work.

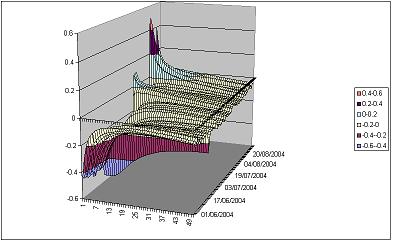

So I did what I ought to have done in the first place and drew a few pictures. Below, I’ve plotted a chart of volatility against price. The purple dots represent the Black-Scholes value of a binary call with 0.152 years to maturity (ie today’s date until the election) at an interest rate of 1.75% (CD rate), with a strike price of 0.50 (see footnote 3[3]), with the underlying at 0.491 (the current quote for KERR in the vote-share market), for different assumptions about volatility. The blue dots are simply a horizontal line at 0.454, which is the current quote for DEM04 on the WTA market. “BS valuation” refers to “Black-Scholes“, you cheeky kids.

As you can see, the model value gets close to, but doesn’t reach the market value. In other words, there is no value for volatility which can be plugged into the Black-Scholes model and deliver the market price. Or to put it another way, the option is overvalued.

This isn’t a transient phenomenon, either. I put together a horrendous Excel spreadsheet which takes minutes to calculate, but which produces a line like the one above for every day of data in the life of the DEM04 contract. Below, I’ve plotted them as deviations from the market price of the option on the same day. As you can see, these curves typically don’t cross the x-axis; it’s the rule rather than the exception that the DEM04 contract is structurally overpriced.

So what’s going on here? Seasoned finance pros will already be champing at the bit, ready to tell me that the Black-Scholes model is a completely incorrect model to use in this context. Well, chaps, allow me to differ. Fair enough, if I was acting as a market maker in size for DEM04, I would probably want to use a more realistic model. But I simply don’t believe that B-S would give such wildly inaccurate prices; one of the good properties of the model is that it’s surprisingly robust. And further investigation of the data suggests that whatever’s going on here, it’s unlikely that we can explain this all away as “holes in Black-Scholes”.

For one thing, this is a phenomenon which is almost entirely one of the DEM04 contract. The REP04 contract prices perfectly well in a Black-Scholes framework, for the most part. This allows us to get another handle on the extent of the overpricing of DEM04; we can solve the model for the implied volatility of the BUSH|KERR vote-share contract (which must be the same as the volatility of the KERR contract) and plug this number into the valuation formula for DEM04. Below, I’ve charted this (careful; avert your eyes if you’re a Kerry supporter).

As you can see, the yellow line (reflecting the “fair value” of DEM04; I’ve put this on the right hand scale for some reason) is way below the blue line (its market value). Don’t pay too much attention to the frightening drop-off in fair value in the last few days; the REP04 winner-takes-all contract has risen much faster in value than the BUSH vote-share contract, a phenomenon which could only be justified by a sharp drop in implied volatility[4], which drastically reduces the fair value of DEM04.

In any case, don’t pay much attention to that chart at all because it’s very badly drawn and poorly laid out it’s clear that any attempt to work on the basis of consistency between the DEM04 and REP04 prices is doomed to failure. The two markets are simply not consistent.

Why so sure? Well, they don’t obey a basic and obvious parity relation. Think about it this way. If you were to buy one DEM04 contract plus one REP04 contract, then you would have a portfolio which would pay out $1 for certain in November. How much would you be prepared to pay for this portfolio? Well, basically one dollar, minus the interest that you could have earned by not buying the portfolio and leaving the money in the bank. So in other words, the difference between the sum of the value of (DEM04 + REP04), and 1.00, is the implied rate of interest which one earns in the financial universe of the Iowa Electronic Market.

I’ve plotted this implied money rate below:

I hope it’s clear. In general, over the last three months, the Iowa Presidential Election Winner-Takes-All market has been pricing on the basis of a negative nominal interest rate. This is not consistent with most concepts of market efficiency.

(as an aside, really astute financial econometricians will right now be screaming about “bid-ask bounce”. The idea here is that the chart above has been plotted using closing prices. However, if the last trade of the day in DEM04 was a buy and the last trade in REP04 was a sell, you shouldn’t really just add them together without making an adjustment for the bid-ask spread in the IEM. This is a fair enough point, but I checked that it doesn’t make a qualitative difference. As I sit here typing, the WTA market has bids of 0.454 for DEM04 and 0.556 for REP04. That means you could sell one of each and get an interest-free loan of a buck.)

So what does this all mean?

Well first, on a practical note, it seems to me that if you want to back the Democratic candidate in the 2004 Presidential elections, you should do so by selling REP04 rather than buying DEM04, and vice versa; this way you take advantage of the fact that option premium is overvalued in DEM04 relative to REP04.

Second, on a more theoretical basis, to my mind this is, unless I have made a howler somewhere, more or less conclusive proof that the IEM is not “efficient” in the financial economics sense of the term. A market in which basic parity relations are not observed is not efficient. One can make all sorts of excuses about the amounts of money at stake, the restricted universe of traders, the fact that short-sellers on IEM do not have full use of funds, etc, but the plain fact of the matter is that the prices on IEM are not consistent with the time value of money.

Third, we can pick up some clues as to what’s going on here from the prices themselves. Although the parity relation does not hold, casually going through the numbers suggests to me that, most of the time, the mid-price of DEM04 plus the mid-price of REP04 adds up to 1, near enough. So there’s a sort of parity rule being enforced by the market participants. That suggests to me that pricing here is being driven by a social convention that the prices ought to reflect people’s estimates of the probability of Kerry or Bush winning. This isn’t how stock options are priced. Financial options are priced on the basis of Black-Scholes and similar models, via an arbitrage pricing argument. Donald Mackenzie studied the sociological process by which financial markets moved from a “probability-pricing” norm to an “arbitrage pricing” norm, and this doesn’t seem to have happened in the IEM (yet; I’ve not entirely given up on my program-trading operation!)

This suggests that James Surowiecki is right and Robin Hanson is wrong on the way in which “information markets” of this kind work. (Update: In comments below, Robin Hanson argues pretty convincingly that this is a pretty egregious caricature of his views. Sorry Robin.)In comments to my review of James’ book, the two of them outlined the difference in their views. James fundamentally thinks of markets as a way for people to “vote” and aggregate their views, with any predictive power they have coming from the fact that they’re a kind of crowd. In particular, for James Surowiecki, markets are just a handy way of organising information aggregation; voting and other ways of summarising crowd opinion might work just as well.

Robin Hanson, on the other hand, appeared to be giving a much more particular role to markets as opposed to any other kind of social organisation. He commented that the reason why markets generated information was ” simple idea that anyone who notices a mistake in the price of a speculative market can make money by fixing that mistake.” To me, this seems like he’s committed to a view that efficiency in the sense of obeying parity conditions is the mechanism by which markets gather information.

This seems like a trival distinction, but it has big practical implications. In particular, if you believe in something like Robin’s view, then you would say that the maximally informative market prices are the most recent ones (because any difference between the prices and the state of the world is most likely to have been arbitraged away). If you believe in something like James’ view, then you might say that a more informative view of the opinion of the crowd might be a moving average of, say, the last five days’ trading. Personally, I’m still something of a sceptic about whether ‘toy’ markets of this kind really deliver the goods at all, and I must say that this exercise hasn’t exactly made me a believer[6]. But it seems to me that if markets like this work at all, they have to work under the Wisdom of Crowds model rather than the Theory of Sharks. And since all the big financial markets operate on the basis of “sharks” and arbitrage pricing, we need to separate them in our minds from toy markets like this; markets which don’t have a Hayekian reason to exist shouldn’t draw credibility from markets which do.

Footnotes:

[1]I promise that this system was in profit when I stopped the experiment; I moved jobs and left all the files behind. My guess is that it would be in loss at the moment, since it seemed to be pretty structurally long Kerry.

[2]Basically, the WTA contracts can be considered to be options (specifically “cash-or-nothing” binary options) written on the vote-share contracts with a strike price of 0.50. Option prices depend on the anticipated volatility of the underlying, so the “implied volatility” is the volatility number that you plug into the formula to make the model price consistent with the market price.

[3]As discussed here, this is consistent with the contract specification. The Iowa vote-share market is for a two-horse race, and the “winner” for the purposes of the WTA contract is the winner of the Iowa VS market. The IEM actually paid out on Gore in 2000 for this reason.

[4]As in, loosely speaking, the Bush contract is currently “in the money”, so volatility in the underlying hurts the binary option more than it helps.[5]

[5]Readers may think that this divergence between the vote-share and WTA contracts is unlikely to reflect a genuine decrease in uncertainty about the vote-share and may represent an investment opportunity. Since CT isn’t in the business of giving advice, readers who want to pursue that line of thought are on their own.

[6]A lot of the problem is that it simply isn’t profitable enough to arbitrage away the breaches of parity, unless you’re doing it just for the fun of proving a point. But I don’t think this is the only problem. And furthermore, even if it was the only problem, it appears to me to be a more or less insoluble one, unless we really believe that in the future we will live in a world where material proportions of peoples’ savings will be diverted away from productive enterprise and into these zero-sum games.

[7]I hereby claim the CT title for “Most Footnotes”

[8]And “Most Gratuitous Self-Citations”.

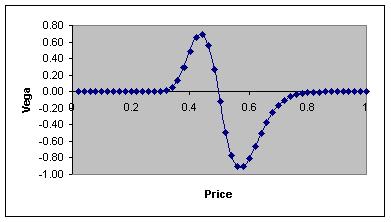

[9]In response to comments, here’s a quick plot of the sensitivity of the option to the volatility assumption (vega). This is plotting the first derivative of the value of the option with respect to volatility. If this doesn’t mean much to you, just laugh at the grotty Excel.

{ 1 trackback }

{ 55 comments }

Kieran Healy 09.08.04 at 5:04 am

That’s a cool analysis. I await the reactions of finance-types with interest. In the meantime, I will imagine the migraines you would give to “Bill Cleveland”:http://cm.bell-labs.com/cm/ms/departments/sia/wsc/ or “Ed Tufte”:http://www.google.com/search?q=edward+tufte&ie=UTF-8&oe=UTF-8 if you showed them any of those figures. Especially the second one.

dsquared 09.08.04 at 5:10 am

This post is also available as a Powerpoint presentation :-)

FWIW, by the by, Tradesports has gone the other way; the implied interest rate there is more like 9.8%. Which implies that you might be able to make decent money by doing the round trip.

Anyone with an account on both IEM and Tradesports, btw, you can buy Kerry in size at 0.41 on TS, so given that you can sell at 0.454 on IEM, there might be about twenty bucks in doing so.

Kieran Healy 09.08.04 at 5:11 am

You should really write this up as a paper.

David Sucher 09.08.04 at 5:22 am

I haven’t even bothered to read your post (and won’t) because the issue of importance is not the horse race and the valuations as of today but who indeed should win. This is not a game, my friend. There are real things at stake. You may or may not have any insights into the likely outcome on Election Day. But even if you are correct — so what?

Only if one is a technocrat, a mechanic, a clerk, would one focus so closely on what other people think. (Which is the essence of markets, obviously.) There are genuine issues in this election and paying attention to “gaming” the election is not on point.

dsquared 09.08.04 at 5:27 am

In a way, I admire your dedication to the purity of the electoral process. But since I can’t vote in US elections, the question of who will win is at least as important to me as the question of who should win.

Plus there’s a chance to make a quid or two, which in the event of Bush winning, should at least buy some beer to cry into.

Katherine 09.08.04 at 5:55 am

As far as crying into beer goes, my husband and I were talking the other day about this question:

is there a single country in the world where a majority or plurality of citizens want Bush to win?

Obviously you can knock off Canada & all of Europe. We figured maybe Israel and maybe Saudi Arabia, with the first a probable yes and the second a probable no (note that we’re talking about the whole population of Saudi Arabia, not just the ruling family). But it seemed totally plausible to us that there might be no such countries.

Again, I’m talking citizens, not leaders.

dsquared 09.08.04 at 5:58 am

The Marshall Islands always votes with the US and Israel in the UN General Assembly on votes when nobody else does … maybe them?

I’d also hazard a guess at Kuwait.

Katherine 09.08.04 at 6:07 am

Kuwait is probably the best guess so far, actually.

CalDem 09.08.04 at 6:19 am

Daniel, you need to go to the website and buy a copy of matlab forthwith, its much more straightforward and its graphics are a 1000X better than excel.

Andrew Boucher 09.08.04 at 6:20 am

“Anyone with an account on both IEM and Tradesports, btw, you can buy Kerry in size at 0.41 on TS, so given that you can sell at 0.454 on IEM, there might be about twenty bucks in doing so.”

Exactly why the market is not efficient ! No one gives a toss. If the IEM accepted credit cards (they only accept personal checks in USD), if they had a larger max (I think you’re limited at 500 USD), etc. then maybe some people would care about arbitrage and these markets would begin to have some semblance of efficiency.

Next time start a market at your home, invite your friends, and see how efficient it is…

Also note the contracts are probably not exactly the same and, even if they were, you still have “term sheet” risk – that even though you think they are the same, there’s some technical detail which you have overlooked that means they are not.

praktike 09.08.04 at 6:36 am

As someone who took Tufte’s seminar, I have to say that he would flunk you. I didn’t learn much in the way of statistics, but I learned to make my graphs purty. Too much chartjunk!

Alex 09.08.04 at 6:40 am

Generally, binary options carry with them very little sensitivity to volatility (in options parlance the ‘vega’ is low). Hence the flatness of the pink line in most vol situations.

The anomaly you identified is almost certainly due to discounting, not vol. IEM bundle values are not discounted for cost of funds, as I imagine your pricing model would be.

Trying to arb the IEM would be fun if the contracts were big enough. As it is there’s a $500 cap — not enough to make it worthwile.

dsquared 09.08.04 at 6:57 am

Alex: But a binary option that’s near the money has really weird vega; it shoots up then shoots back down again. And the way that IEM is set up, both contracts are almost always near the money.

I don’t understand what you mean by saying that the IEM bundles aren’t discounted; they pay off either $1 or nothing the day after the election. It’s not exactly hard for players in the market to do the discounting?

Andrew: How big do you think a market would have to be before it started to be efficient? (btw, your friends might not jump on pricing errors like this, but mine would like ferrets on a sausage. And the IEM are meant to be played by business school students!) Given that IEM is the oldest of its kind, how likely is it that any similar exercise would achieve that scale?

dsquared 09.08.04 at 6:59 am

btw, I’m not going to defend all those charts, but I think that the second and fourth one obey at least some principles of use of ink, data density etc.

Sebastian Holsclaw 09.08.04 at 7:33 am

Interesting post. You are probably right about the difficulty of getting good market information out of a toy market.

Chris 09.08.04 at 7:35 am

I’m unlikely to ever call a graph from Excel beautiful, but I think we should go a bit easier on these examples. They could be better labelled, and there were better options than a 3D plot for number 2, but the plots convey a lot of information, and make clear contrasts between BS and IEM behavior. I think Tufte and Cleveland would say that these are the most important things.

I second Kieran: this should become an article. It would be better than several I’ve seen published on IEM.

Andrew Boucher 09.08.04 at 8:32 am

d^2. With given conditions I’d become interested if the expected payoff were north of 1000. If credit cards were accepted (and you could set up accounts instantly), then I’d probably be willing to arbitrate the first time for 0 (i.e. just for boasting rights), but I’d probably need to make > 100 Usd per arbitrage before I become interested to help maintain market order (!). I’d expect my levels are on the low level, so I’d probably be one of the first to arbitrage.

abb1 09.08.04 at 11:47 am

Is there a possibility that this market is manipulated by the Bush and/or Kerry campaigns?

Wouldn’t it make sense for a compaign to open a large number of accounts, buy all or most of their candidate’s contracts and then trade these contracts at artificially inflated prices between their accounts. It would have a certain propaganda value for them, right?

James Surowiecki 09.08.04 at 3:46 pm

Fascinating post, Daniel. I’d been struck by the lack of parity relation in the WTA contract, and I’d wondered it was a result of something like people using a probabilistic rather than arbitrage model, but this is just an excellent proof of it. A couple of things I wonder about:

1) Given what seems to be a deep-seated bias against short-selling, it seems to me that people who believe in a candidate’s chance of winning would be far more likely to register their view by buying their preferred candidate’s contract rather than selling the opponent’s. That makes me wonder whether the two markets (DEM04 and REP04) are in some sense self-contained (even though in theory they’re two sides of the same coin), and reflect the judgment of the market — informed, of course, by the price in the other market, which is why the relation stays close to 1 — of the candidate’s chances of winning.

2) What is the proper relation between the verdict of the vote-share market (which happens to be the market I’ve paid most attention to, even though it’s much smaller in dollar volume) and the verdict of the WTA market? In other words, if the VS market is predicting that Kerry is going to get 49% of the vote, is there a price in the WTA market that should follow from that?

3) I think abb1’s point about the possibility of manipulation is an interesting one, if only because the IEM has gotten so much more attention this year. On the other hand, if the markets are obeying a rough parity convention, that would seem to suggest that manipulation isn’t really at work.

Alex 09.08.04 at 4:10 pm

dsquared –

the no-arb conditions of the B-S pricing model are violated by the IEM itself, which as described exhibits arbitrage conditions all the time. the two binary contracts in the given example are worth more than $1.00, so selling the package will in fact yield an automatic profit (albeit miniscule.) Thats one problem with the analysis.

The second problem is more significant.

re: carry —

The model presumes interest is earned by the seller, and paid by th buyer. But in the case of IEM, no interest is earned by either party — funds sit latent in your account earning no interest until they are spent. $1 spent on a WTA bundle earns no more interest than an unused buck sitting on account. And selling the package at 1.00 will earn no extra carry for the seller. Hence no discounting effect should be expected (nor occurs) on the IEM though it is certainly presumed by the conditions of the pricing model itself. Hence the anomaly — the pink line cannot reach the IEM value because it thinks there should be discounting applied, though in IEM-world interest is irrelevant.

binary options in ordinary vol environments with some time to expiry generally have very low vegas. Close to expiry or in a low vol environment you will see the vega change as you cross the strike as you describe, but attributing any meaningful pricing effect to vol in this example is mistaken. With any time to expiry vol is irrelevant to binary prices in most vol regimes.

A trivial point: since the underlying vote share represents a percent of 100, isn’t a lognormal pricing model such as B-S inappropriate? B-S and Black76 presume an unbounded distribution (ie the underlier could conceivably go to a zillion)– unlike a vote share market which is bounded by 0 and 100.

mighntn’t you use an interest rate or fx model with similarly bound underlying distribution?

Chance the Gardener 09.08.04 at 4:22 pm

Tufte would and should have a problem with the designers of Excel instead of the users of such product.

To sum: ‘You can’t polish a turd.’

Having said that, the more ‘meta’ we get from the actual person-pulling -the-lever-and-casting -the-vote, the less I put stock in the results. Sure, the fifteenth derivative of the obscure datum points to whatever, but until the new president is sworn in, all bets are off.

To me, all these models make no sense, because people don’t always vote rationally, so it is really impossible to tell. Does your model include Breslan? Zell Miller’s speech?

And really, you can toss all this away statistically by saying that the kind of people that are funded enough to play around with these things are generally the same people that vote republican. And since the money involved seems to fall under the threshold of ‘I will buy this because it is my TEAM! GO TEAM’ I really can’t put much stock into people really following a rational financial interest over the visceral.

Alex 09.08.04 at 4:29 pm

“Is there a possibility that this market is manipulated by the Bush and/or Kerry campaigns? ”

From the .41/.454 example it would seem the Kerry folks might be doing just that (!)

Tom B-L 09.08.04 at 4:37 pm

I’m not sure whether this is still the case, but the prospectus (see “CONTRACT BUNDLES”) suggests that the IEM themselves will buy/sell you a bundle consisting of one BU|KERR and one KERR for 1$; this (together with the lack of interest earned on IEM cash a/cs pointed out by alex) might explain the violation of the parity rule.

(This also suggests an even easier arbitrage oppotunity: short the bundle of KERR and BU|KERR, invest the 1$ proceeds, and pay your $1 come election day. You pocket the interest on the $1.)

tom b-l 09.08.04 at 4:41 pm

(In other words, it’s not just the market participants that have “forgotten” about the time value of money; the whole system ignores it…)

Jason 09.08.04 at 4:53 pm

I know of at least one person attempting to manipulate the market. That $500 limit is really small.

Alex 09.08.04 at 4:59 pm

I would guess that there is attempted manipulation in both directions. $500 is not so high a cap , so pocket depth is less significant than # of accounts.

Tradesports/UK odds are a bit harder to explain away, as real money can be involved.

Ben 09.08.04 at 5:57 pm

The http://www.oddschecker.com/oddschecker/mode/o/card/cc8859x/odds/243698x/sid/377975>UK market is showing a similar picture as the US: odds lengthening on Kerry and shortening on Bush, with Bush a clear favourite.

nnyhav 09.08.04 at 6:15 pm

Volatility smiles at fat tails; here’s the skinny:

1) Forgoing interest is a precondition of participation in this market. r=0.

2) Distribution assumption is much worse than prior comment indicates. Whilst mean may move, tails diminish both ways, and are probably pegged above and below (certainly at 0 out of range). So from symmetrical (though non-gaussian) distrib at even odds, skew moves with mean cuz the tails don’t.

Even with such model adjustments, market efficiency seems dubious.

dsquared 09.08.04 at 7:25 pm

Alex; but if you wanted to have a bet on KERR, say, you could finance it out of the proceeds of selling DEM04+REP04. The funds aren’t locked up, and even if they were, I can’t see how this would justify a negative time value of money. Also, I’m not sure what you mean by the “Black-Scholes no-arb criterion” – arbitrage free pricing is not a quirky assumption of B-S that can be relaxed, it’s a fundamental axiom of pricing and certainly necessary for markets to be considered efficient.

On the subject of vega; graph the function (actually, I’ve got a chart here so I’ll bear the laughter of the crowd and upload it). With 0.2 years to expiry, money rate 1.75%, strike price 0.5, vega goes from 0 to 0.8 to -1 to 0 as the price goes from 0.4 to 0.6.

Nnyhav: As I mentioned to Alex, people who are speculating in this market are presumably doing so with real money. If they’re accepting a zero interest rate to do so, that’s not efficient markets.

Furthermore, the distributional assumption is only going to make things worse. Any changes you make to the distribution to reflect the reality of the distribution of vote shares are going to tend to make the distro less leptokurtic, not more, which would imply even lower fair option premia and make the mispricing larger.

dsquared 09.08.04 at 7:28 pm

James; my first chart is meant to show the answer to your question 2. Every figure in the VS market (plus a time to maturity and an interest rate) is associated with a schedule of consistent prices in the WTA market, one for each possible assumption about volatility.

dsquared 09.08.04 at 7:36 pm

Lads: I just recalculated the spreadsheet on the assumption that the prevailing rate of interest for IEM purposes was zero, and it didn’t make much of a difference to the surface plot; the pricing anomaly is still there. As the bar chart suggests, we would need to find some principled justification for a negative nominal rate of interest (and, just to forestall convenience-yield type explanations about the price people are prepared to pay to be in the IEM action, we’d also need a theory of the fluctuations in that negative rate of return) in order to explain the problem in this way.

Matt Brubeck 09.08.04 at 7:41 pm

dsquared: “Anyone with an account on both IEM and Tradesports, btw, you can buy Kerry in size at 0.41 on TS, so given that you can sell at 0.454 on IEM, there might be about twenty bucks in doing so.”

I think you’re looking at the “Presidential Election Winner” claims on TradeSports. You should by looking at the “Most Popular Votes” claims instead, since that’s how the IEM Winner Takes All market is judged.

In the TradeSports popular vote market, bids for Kerry start at 45%, just like the IEM WTA market.

dsquared 09.08.04 at 7:44 pm

Matt is entirely right and illustrates both a) how important it is to be painstaking and punctilious in keeping track of the different contracts and b) in view of this, why I am uniquely ill-suited to the job.

Though the 4% implied probability that the electoral college will screw the American public looks like an overestimate to me … so maybe I will set the controls for the heart of Oxymoronia and declare it to be a “statistical arbitrage”.

Alex 09.08.04 at 7:53 pm

By no-arb I am taking for granted the IEM markets are inefficient — hence the ability again and again to earn small money selling (and less frequently buying) the WTA bundle at market. This function should be automated by the IEM but for some reason isn’t. It would be more instructive to strip out the option component and describe the floating market value of the package and see what it’s implied IR is. i see that sometimes the package exceeds 1$ — my conclusion is that on the IEM it is mechanically simpler to buy than to sell, occasionally inviting trivial arbs from time to time (due to lazy buyers), nothing more systematically meaningful than that.

as for continually withdrawing your money from the IEM in order to invest, yes technically possible but incredibly cumbersome and swamped by fees, so IMO ultimately irrelevant. PRACTICALLY (net of fees, time lag, postage) no interest may be earned on credit balances, so i wouldn’t expect it to play a role in pricing. Efficient? no, but neither is a clearing account on an exchange where different yields are earned/paid for credit and debit balances.

you are missing a vol. assumption in your vega figs but my trivial point there is that vega is usually unimportant when looking at binaries. Im not sure in what units your vega variable is expressed so its hard for me to judge, but in a high vol market (as the kerry market almost certainly is, 2% daily move translates to ~32-38% vol) with 3 months to go vega should be negligible on both sides. The flatness of your pink line above 20% i think validates this. again, very trivial — considering the package price would eliminate any vol- (or distribution-) induced headaches.

dsquared 09.08.04 at 8:10 pm

Alex; the units on the horizontal scale are the price of the contract in dollars (from 0.02 to 1.0) and the vertical scale is the pure number which is vega. I used a vol of 0.2; if I put in your suggestion of 0.4 the range is plus 0.5 to minus 0.75, none of which seem trivial to me. Remember that vega of binary options changes dramatically with moneyness; as I say, the fact that the IEM binary contracts are almost always very near the money means that vega matters a lot more than one might think.

The implied interest rate from the package is shown in the bar chart on the fourth graph down; admittedly it’s drawn up based on closing prices rather than genuine contemporaneously tradable bids, but that’s as good as we’re going to get unless someone fancies writing a spider program to generate high-frequency data.

dsquared 09.08.04 at 8:13 pm

erratum; of course vega isn’t a dimensionless number but I’m tired and I can’t be bothered working out what the units are. Dollars per standard deviation or something.

dsquared 09.08.04 at 8:25 pm

Or in other words (and I’ve just been playing around with this in a spreadsheet to see what happens), moving that vol assumption from 38% to 48% can make a 2 cent difference in the value of the WTA contract if the VS contract is trading between 0.495 and 0.51 – elsewhere, Alex is correct and it doesn’t make much odds. This strikes me as a region of interest since empirically, the VS contract does spend quite a lot of time in this range, and 2 cents difference is in this region the difference between favourite and underdog. It looks worth a bit more attention, though I agree that Alex is right that, further away from the money, vega is less important than I thought.

tina 09.08.04 at 8:32 pm

Katherine,

A poll of 35 countries around the globe has the Phillippines with the only majority favoring Bush, and Poland and Nigeria as the only two with pluralities favoring Bush. All others favor Kerry.

I’m not sure if Kuwait is included or not. I don’t have the data but here’s the story from the Int’l Herald Tribune.

nnyhav 09.08.04 at 10:46 pm

> Furthermore, the distributional assumption is only going to make things worse. Any changes you make to the distribution to reflect the reality of the distribution of vote shares are going to tend to make the distro less leptokurtic, not more, which would imply even lower fair option premia and make the mispricing larger.

d^2: You’re thinking too standard normal. If the distro is deformed in the manner I describe, the “in the money” tail is compressed, the “out of the money” expanded, making the latter appear more leptokurtic locally. (Volatility is no longer a scalar measure, becoming dependent on location of the mean.) The resulting asymmetry may or may not account for the apparent mispricing, but certainly reprices in the appropriate direction. It’s not meant to “reflect the reality of the distribution of vote shares” (suggesting some empirical parameterisation), only to reflect the reality of certain constraints thereon.

old maltese 09.08.04 at 11:48 pm

tina —

If I were a Dane knowing only what my local media are telling me, ABB would seem the only rational option.

Robin Hanson 09.08.04 at 11:54 pm

Why do you keep trying to put words in my mouth? Last time you said I misread Hayek, when I don’t discuss Hayek. Now you say I’m committed to the view that no one should ever find arbitrage opportunities in information markets. But I’ve never said any such thing. And I’m not even aware that James Surowiecki and I disagree on anything in this area. (Why not call me and talk, if you want to know what I think?)

Let me make an analogy. Private bounty hunters have an advantage over public police in having a stronger incentive to catch their targets. Does this mean bounty hunters always catch every target on the first day? Of course not. It just means that bounty hunters catch people faster and cheaper on average. Similarly, that fact that people can make money by fixing mistakes in information markets just gives those markets one advantage over mechanisms, like voting, which lack this feature. Not every mistake will be found and fixed – the effort to do this is often more than the reward offered.

I’m open to the idea that a moving average might sometimes be more accurate, and even looked into that possiblity in our recent laboratory experiments. Even though these markets were very thin and inefficient, however, it still turned out that the last price was at least as accurate as moving averages.

I have consistently proposed that information markets be subsidized by those who want the information. Subsidized markets are not zero-sum. If no one will pay to induce information on a topic, then we may well not get much information on that topic.

Alex 09.09.04 at 12:25 am

“In other words, if the VS market is predicting that Kerry is going to get 49% of the vote, is there a price in the WTA market that should follow from that?”

I suspect no such inference could be drawn without using some speculative anticipated volatility of VS (as would be needed for the n(D1) expression in B-S that means the same thing as the binary.)

Phill 09.09.04 at 12:31 am

I think you are way off here. The prices of options may reflect supply and demand. The most obvious explanation of the price of the Kerry contract is that large numbers of people realize that the cost of a Bush victory is another four years of utter incompetence. These individuals are therefore taking the rational step of insuring themselves against a Bush victory.

The same effect is seen in insurance markets. I buy insurance on my house even though I neither expect nor desire the house to burn down. I pay substantially more for that contract than the probability of a total loss times the insured value.

Alex 09.09.04 at 12:31 am

whoopsie thats N(d2) for the binary .. sorry math guys.

James Surowiecki 09.09.04 at 1:59 am

I should also say, with regards to the moving-average/last-price question, that I think — as I argue in my book — that most of the time the market price in fact reflects the collective judgment of the crowd of investors. (The price of the last trade before market close probably doesn’t, but most of the time the two will be very close.) So I don’t think the distinctions between information markets, financial markets, parimutuel pools, or sophisticated voting systems are really all that important. In the terms Daniel sets out at the end, I think all markets are, roughly speaking, information markets. But Daniel — and most corporate-finance theorists — disagree with me on this, so I’ll be satisfied with the idea that the IEM, at least, is aggregating probabilistic forecasts.

The more substantive question has to do with Daniel’s implicit argument that in the absence of an opportunity for real profits, no one will invest any money in these markets. That may be the case, and one way around it is to subsidize them, as Robin Hanson suggests. But I’m unconvinced that the markets need to be real-money markets in order to aggregate useful information. A recent comparative study of the performance of the Newsfutures (which is a play-money market, with prizes for the best performers) and the Tradesports markets in NFL games found that the prices in the two markets were about equally good predictors of outcomes. (They were both, unsurprisingly, very good predictors.) Now, the NFL is perhaps a special case, since there’s lots of public information and there a lot of people who devote a lot of their free time to keeping up with the game. But it suggests that in at least some circumstances — certainly, I think, within many organizations — markets or other aggregating mechanisms can produce valuable forecasts even in the absence of the opportunity for material profits. (I think there do need to be rewards for good performance, but I think these could take a variety of forms.)

Jon H 09.09.04 at 2:20 am

Back in the 80’s, there was this thing on Friday nights on MTV, where they’d play two videos and take votes on which was better, via calls on a 99 cent 1-900 number.

That strikes me as being just as much a ‘market’ as the Iowa electronic market.

The only difference is that MTV never promised a financial payoff. It only offered an emotional payoff in the form of having your favorite video “win”. Yet real money was at stake, in the form of the charge on your phone bill.

I think that the Iowa market actually operates in a similar way. I suspect many people who participate aren’t actually doing it to get a financial return, and they aren’t concerned about the fate of their small ‘investment’. They’re just doing the equivalent of voting via a 99 cent 1-900 number.

Jon H 09.09.04 at 2:36 am

dsquared – if you write this up as a paper, you really ought to redo the graphs.

I suggest using little Bush heads and Kerry heads to mark the data points.

nnyhav 09.09.04 at 2:51 am

Still, all this going on about the time value of money, and no one’s seen fit to equate it to neglecting the cost of Kerry?

Kieran Healy 09.09.04 at 3:43 am

Here’s a “different version of the trend surface”:http://www.kieranhealy.org/files/misc/dem04.pdf. A bit more discussion “here”:https://www.crookedtimber.org/archives/002466.html

Sven 09.09.04 at 4:25 am

In perusing CSIS’ latest report on Iraq, I noticed The Wisdom of Crowds was used in designing the methodology for measuring reconstruction efforts. Berry interesting…

Alex 09.09.04 at 4:31 am

” one’s seen fit to equate it to neglecting the cost of Kerry?”

ba dum bum.

I re-read this post and I suspect more and more the question is being overcomplicated by unnecessary option analysis. I would bet a similar study of the market-settled package would yield a similar “negative carry” for the basic reason that newcomers to market tend simply to buy or bid one or the other contract instead of buying the package and selling an unwanted overpriced component. Hence the package is routinely priced 1 or 2 cents over parity purely by accident, yielding the observed ‘negative carry.’

globecanvas 09.09.04 at 5:02 am

I agree with Alex’s summation. Putting on a synthetic short is at least two transactions, and people come to IEM to buy their dreams, not to buy the world and sell back their nightmares.

Mats 09.09.04 at 11:36 am

DD: “[including bid-ask spreads does not] make a qualitative difference.”

-Well yes, if you don’t think there is a qualitative difference between borrowing a dollar at double digit negative interest rate and borrowing it at zero, as in your example.

Besides, as noted above, order depth is really so so. My feeling is that you would probably earn more as a market-maker than an arbitrageur on these betting exchanges.

dsquared 09.09.04 at 3:46 pm

Mats: it was zero on the precise occasion when I typed that. I’ve seen mid-single digit negative rates on the bids on a couple of occasions in the past; the -20% is almost certainly a figment of the data.

Alex: In many ways I agree with you, though the option analysis is interesting because it shows that the pricing anomaly in the package is entirely concentrated in the DEM04 contract. This is quite interesting from the point of view of the sociology of the IEM, because I think that’s the market’s way of telling us that DEM04 is a superfluous contract; since being short one contract is equivalent to being long the other, it looks to me as if REP04 is the one that gets priced sensibly, and DEM04 just floats around. My advice to the IEM people would be to not divide up the liquidity pool in this way and only have an INCUMBENT04 contract.

Patri Friedman 09.10.04 at 7:32 am

Over at Catallarchy, I’ve blogged a comparison of markets and crowd polling as opinion aggregators. I think this explains why IEM is not efficient, and why Tradesports and similar markets still can be.

Comments on this entry are closed.