Ireland’s recent €85bn bail-out package negotiated with the IMF and the EU is discussed in terms that verge on the apocalyptic. The rescue was supposed to serve as a break against the wildfire of market bondholder panic. And yet the upward trend in Portuguese bond rates has scarcely been slowed. Beyond Portugal  is the much larger Spanish economy. Portugal, like Greece and Ireland, could probably just about be rescued within the terms of the current emergency scheme. It is becoming increasingly possible that the bond markets may make it too difficult for the Spanish government to refinance its loans and to raise new money on government bonds. If this were to happen, the European Financial Stability Fund would come under extreme pressure. And worse, if it is not possible to restore confidence in the stability of the Euro, there seems little reason why other countries may not also be in trouble. Spain is now where the line in the sand must be drawn. But we have heard this before. If Spain is vulnerable, why not Italy; and if Italy, why not Belgium, perhaps even France. Little wonder that the imagery of contagion, of financial plague, is brought into play.

The suddenness of the Irish deal has taken public opinion by surprise, causing shock that we have been plunged into this regime of austerity, and a smouldering anger about the terms on which the deal has been done. The terms of the bail-out will transfer all the hardships onto the taxpayers and citizens: reactions include the views that we have been held to ransom, we cannot afford this rescue package, it is a bad deal for Ireland.

Ireland’s fiscal crisis is largely caused by the collapse of the house price bubble and over-reliance on revenues from construction-related activities. This is bad enough, but by itself it would be difficult but manageable. The millstone around the neck of the Irish people is the vast scale of the crisis in the banking sector. Ireland’s banking crisis is not primarily about complicated and risky financial products: it is a common-or-garden result of reckless lending for property development and an inadequate regulatory regime. Between 2004 and 2007, the banks had escalated the scale of their lending to construction and property development enormously. When financial meltdown was imminent in September 2008, the government undertook to guarantee all of the banks’ losses, bondholders as well as depositors. In what is now widely regarded as a terrible mistake, the government in effect socialized the enormous private debt of the banks.

The true picture of what is entailed has been slow to emerge. The government’s attempts to shore up the banks have not involved outright nationalization, but the creation of a National Asset Management Agency (NAMA) to transfer the bulk of the banks’ non-performing property-backed loans into a special purchase vehicle, at a discounted rate. This amounts to indirect recapitalization of the banks. The total cost of Nama-type loan loss is now estimated at €66 billion. This is, in effect, half of GNP (the best measure of the taxable resource base of the Irish economy), which in 2009 amounted to €131.2bn. Mortgage and personal loan losses have not yet come fully into focus, but may amount to an additional €25 billion.

The present government, a coalition between the dominant centre-right Fianna Fáil and the Green Party, must go to the polls soon, and they will certainly be trounced. But unpopular though it is, the government was adamant until almost the last moment that it did not need or ask for the rescue package. Borrowing needs were fully met until mid-2011, and government had no need to go back to the bond markets. ECB as well as European Commission representatives had been on an extended visit to the Department of Finance, inspecting plans for the budget due on 7 December, in line with the strengthened fiscal oversight practices in the Eurozone. EU Commissioner for Economic and Monetary Affairs Olli Rehn had declared himself happy with the plans he had seen. Austerity measures were projected to take some €4bn out of the economy as part of the planned fiscal consolidation strategy. This was intended to ensure conformity with the Stability and Growth Pact requirements of 3% deficit by 2014.

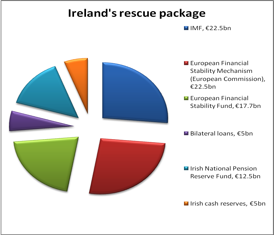

Yet Ireland is now committed to an IMF-EU rescue package worth €85bn over the coming years, to fund both government spending and to support the costs of sorting out the crisis in the banks. It all happened very quickly, and indeed one government minister said they were bounced into it. The terms are set out in the government’s new four-year fiscal plan. The interest rate involved is not low, at an average of 5.87%. The total fiscal contraction will come to €15bn, though the deadline is now extended until 2015. The December budget alone will take out €6bn in a mix of spending cuts and tax increases. This is tougher than anything that had been envisaged so far. In addition, the National Pension Reserve Fund, a rainy-day measure set against future public pension liabilities, is to be used as part of the bail-out package. Most controversially from the point of view of Irish taxpayers, while these public assets are to be committed to the front line of bank recapitalization, the banks’ bondholders are not to be required to bear any losses. The most equitable adjustment measure, from the point of view of the Irish taxpayers, would have required some element of writing down outstanding debt through an orderly restructuring, that is, burning the bondholders. But this could damage government’s capacity to raise future funds through borrowing; government ministers stress that they really had no option in this. Yet there is palpable anger in Ireland at the outcome which ensures that the banks will be bailed out while the cost is to be borne in full by the taxpayers.

The composition of the rescue package is shown below:

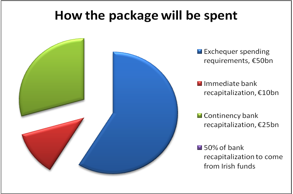

Most of the funding is to be committed to supporting government spending. A chunk will go straight into the banks immediately, while another chunk will be held as a reserve.

The way the rescue package is to be used is shown in the figure below:

Governments must adopt a whole series of highly unpalatable measures at least until 2015.Yet the plan will only work if real GDP grows by 2.75% each year. The depressing effect of extreme fiscal austerity makes this target look extremely difficult.

How did it come to this? And given the size of the intervention, why have the bond markets not been assuaged? Ireland was meant to be the firebreak in asserting the primacy of political commitment to the Euro over market irrationality. But this did not work. Instead Ireland got burned.

The explanation has to do with the fragmented sources of authority involved in managing the Euro, and the competing imperatives each of them needs to attend to.

The ECB intervened suddenly in response to the sharp rise in interest rates on Irish bonds, not because Ireland needed the deal, but because the ECB needed to stem uncertainty. It would seem that senior bank bondholders were exempted from taking any share of the pain at least in part because of the scale of the potential exposure of the German banks to Irish losses.

Interest rates spiked because German and French leaders are now openly working toward putting the current emergency rescue measures on a more permanent footing. This will mean involving senior bondholders in unwinding any future defaults, consistent with IMF practices, but the plan will only take effect after 2013. But Angela Merkel’s open speculation now about the conditions for future default had the effect of further unsettling current investors. Moreover, if default is explicitly accepted as a possibility, the Euro could become as unstable as the European Monetary System was during the 1980s.

Angela Merkel has other problems too: German popular opinion is restive about what is seen as a one-way flow of German taxpayers’ money to the troubled periphery. The result is that her public statements, issued for different audiences, seem to lack consistency.

And yet financial difficulties are not a natural phenomenon like disease, nor are they spread through diffusion like fire. Bondholders and investors may exhibit a herd mentality and act from ‘animal spirits’, but they are not incapable of reasoning. Market uncertainties are the aggregate outcome of a host of assessments about risk and about growth.

The European fire-fighters seem to be at least one step behind the game on both of these issues. Bail-outs and safety nets are crisis measures, not for the long term; but planning for a stable resolution regime is causing its own uncertainties. Harsh and even punitive fiscal measures to address what are really financial and not fiscal crises will further depress growth in the European periphery. The only realistic prospect for generating new growth in the Eurozone is if Germany were to engage in demand-enhancing measures, not the fiscal contraction to which is now seems committed. There is little prospect of this happening at the moment.

Europe seems fated to a series of attempted fire-fights, one a time, without any clear prospect of stabilization in view. Meanwhile, Irish citizens look around at their scorched fiscal landscape in dismay.

{ 47 comments }

y81 12.01.10 at 9:48 pm

Why did the Irish government guaranty all bank debt in September 2008? That seems, from this narrative, and others I have read, to have been the first fatal misstep. Even the U.S. Federal Reserve, which is possessed of vastly greater resources, did not go that far. What was the government thinking?

Omega Centauri 12.01.10 at 10:12 pm

To further y81’s question. Obviously the September 08 deal was far too generous to the bondholders, doubtlessly the government misread the situation, thinking if it could temporarily calm the waters the crisis would pass. What are the prospects and costs of “renegotiating” this deal (i.e.

forcing the bondholders to share in the haircut)? I can’t imagine the next Irish government won’t be elected without some sort of a mandate to do that.

Henry 12.01.10 at 10:20 pm

bq. Why did the Irish government guaranty all bank debt in September 2008? That seems, from this narrative, and others I have read, to have been the first fatal misstep. Even the U.S. Federal Reserve, which is possessed of vastly greater resources, did not go that far. What was the government thinking?

This is a question that many people would like to know the answer to. Plausible speculation turns on the intimate relationship between the bank that was about to go under and the political party then in control of government. The justification was that this bank was suffering a temporary little liquidity crisis – but it was reasonably clear at the time that the problem went far beyond that. Fintan O’Toole’s new book has some discussion.

On whether or not the new government can or cannot negotiate a haircut for bondholders, this is the topic of heated political debate. Roughly speaking – the European Central Bank and the Commission (as represented by Rehn) vetoed proposals that bondholders take a haircut in the package deal announced last week. The main opposition party has made noises that it wants to reopen the deal (although it has not, as best as I know, raised the bondholder issue, and I suspect will knuckle under when the time comes). Rehn has intimated that this is not possible. The main opposition party is now claiming that it may be able to reopen the deal after 2011 given ambiguities in the memorandum of understanding, but I suspect that this is mostly electioneering and slogan-tossing rather than action that it intends to deliver on in any serious way.

CMK 12.01.10 at 10:34 pm

What happens after 2015? Is there a possibility that Ireland will need to be bailed out again? If the ‘Four Year Plan’ doesn’t succeed in reducing the deficit to 3%, which appears to be the most likely possibility, where will the state get the funds to provide services thereafter? The apocalyptic tone noted above is perhaps a instinctive recognition that the bailout has just postponed the inevitable collapse of the Irish state as a viable entity i.e. as an entity that tries to combine the provision of services to its citizens as well as serving the interests of the bondholders. After 2015 it might be forced to aggressively defend the interests of the bondholders against citizens.

James Conran 12.02.10 at 12:09 am

One detail worth adding is the extraordinary share of ECB liquidity provision taken up by Irish banks (using Irish sovereign bonds, including NAMA bonds, as collateral) in the last year or so. So the ECB, as well as German banks, was/is in line for losses following Irish default. The ECB’s role in instigating the bail-out came in the form not only of directly pressuring the government but also by its indication that this liquidity support was going to be withdrawn.

John McManus had an interesting piece on the ECB role in the Irish Times a few days ago:

“One of the main differences between how the two-year-old crisis has played out in Europe and America has been the refusal of the ECB to allow any significant bank fail.

It is worth noting in this regard that Jean Claude Trichet rang Brian Lenihan over that fateful weekend in September 2008 to impress on him the importance of not letting any Irish bank fail.

…

[The ECB] has provided liquidity to the Irish system to such an extent that Irish banks account for something like one in every four euro it makes available through its emergency measures…..

…

Now, in order to extract itself from this mess, the ECB has in effect withdrawn its support and said that the Irish taxpayer must now borrow even more money and try – for a third time – to fix the knackered banks so the ECB can get its money back.

The alternative to the Irish taxpayer stumping up – letting the badly broken AIB and Anglo Irish banks fail or default on their bonds – remains resolutely off the agenda at the insistence of the ECB. The reason being the same as it was in September 2008: the Irish banks are systemic in the European context . The big losers if either bank failed are the German, French and other European banks and institution that funded their insane lending sprees.”

http://www.irishtimes.com/newspaper/finance/2010/1122/1224283833586.html

P O'Neill 12.02.10 at 12:28 am

The so-called Honohan report pages 119-136 provides the consensus processology of the guarantee. Prof. Honohan put in enough sentences that the government can selectively quote to defend the decision, but read in its entirety, it tells its own less flattering story. In particular, the extent to which the guarantee sprang from a previous policy priority (no bank failures) that was never fully articulated, it’s breadth (covering all existing debt, not just new issuance), and the way it precluded any resolution of the truly insolvent banks (Anglo and INBS).

piglet 12.02.10 at 12:45 am

christian_h 12.02.10 at 12:47 am

There’s of course another way to get out of the whole problem: inflation. The ECB, being supposedly independent, could just create money.

Barry 12.02.10 at 12:58 am

Another question – from what I’ve been reading (chiefly, here), Ireland is currently being subjected to savage austerity measures, which are driving the country into an actual Great Depression II. Meanwhile the country is being asset-stripped (pension funds!) to pay the bankers who did this.

At what point will either (a) the economy collapse to the point where the government literally has no money to function, and/or (b) the Irish people realize what their government is doing, and are desperate enough to take, well, desperate measures?

Or, to put it shortly, at what point does a revolution happen?

Sabra 12.02.10 at 1:13 am

Can someone compare the fallout on how Iceland handled their crisis v. how the Irish crisis is being handled?

Glyn Morgan 12.02.10 at 1:24 am

An excellent and most lucid account. Thanks.

bob mcmanus 12.02.10 at 1:50 am

9:Or, to put it shortly, at what point does a revolution happen?

When people like you and I become the point of the spear.

P O'Neill 12.02.10 at 2:05 am

#10

Ireland v Iceland, the numbers — 2010 and after are projections.

The basic story: Iceland much worse initially as the banks were transparently insolvent and immediately nationalized, massive currency devaluation, capital controls, and messy dispute with UK and Netherlands over compensation for depositors of Icelandic bank branches in those countries.

Ireland — no immediate nationalization, no currency depreciation, no bank defaults, pundits hailing austerity, and the government using “ICELAND!” as the talking point for why they couldn’t consider any alternative policies.

As the numbers show, hard to tell in 2010 who is worse off, especially as Ireland ends up with Iceland banking policies in slow motion, so it’s not clear what all the intermediate bank shenanigans accomplished.

James Conran 12.02.10 at 2:07 am

I second Christian H’s point. To be sure, German demand enhancement measures would be as welcome as they are unlikely, but we really should be questioning what on earth is going on at the ECB. A good old bout of inflation would be a Godsend but not only is the ECB holding out against QE, it hasn’t even hit the zero lower bound on the ordinary policy rate! And now it appears to be getting uncomfortable with the role of lender of last resort.

john c. halasz 12.02.10 at 2:13 am

“When people like you and I become the point of the spear.”

What? As opposed to the shaft?

bob mcmanus 12.02.10 at 2:30 am

15: What, jch, you’re going to make some other poor grunt take point?

Barry 12.02.10 at 2:32 am

James Conran 12.02.10 at 2:07 am

” I second Christian H’s point. To be sure, German demand enhancement measures would be as welcome as they are unlikely, but we really should be questioning what on earth is going on at the ECB. A good old bout of inflation would be a Godsend but not only is the ECB holding out against QE, it hasn’t even hit the zero lower bound on the ordinary policy rate! And now it appears to be getting uncomfortable with the role of lender of last resort.”

In both the USA and Europe it’s clear now that the economic elites are very comfortable; they can extract money from governments, and then use their cash in poor times to make even more money.

y81 12.02.10 at 3:05 am

“the country is being asset-stripped (pension funds!) to pay the bankers who did this.”

But that’s not what the narrative shows at all. As far as I can see, the country is being asset-stripped–or at least subjected to public sector austerity–to pay the banks’ bondholders. I am not sure who owns the bulk of Irish bank bonds, but there’s no reason to think it’s (i) bankers or even (ii) rich people (who, at least here in the U.S., tend to have barbell portfolios of tax-exempt bonds and equities),

Nabakov 12.02.10 at 3:32 am

“What? As opposed to the shaft?”

or the sniper’s spotter.

john c. halasz 12.02.10 at 3:48 am

@16:

Bad puns and still worse metaphors aside, in the old jargon, there was the distinction between subjective and objective conditions, which seems to have fallen into abeyance. I’ve never been a fan of the vanguard theory, but I think the best that can be done is to continue and sharpen the critique of finance/fictional capital and its associated macro until the shaft sharpens its own spear.

Glen Tomkins 12.02.10 at 5:10 am

“it’s not clear what all the intermediate bank shenanigans accomplished.”

Gave the smart money time to get clear off. Rome wasn’t liquidated in a day, you know.

.

burritoboy 12.02.10 at 5:32 am

” “the country is being asset-stripped (pension funds!) to pay the bankers who did this.â€

But that’s not what the narrative shows at all. As far as I can see, the country is being asset-stripped—or at least subjected to public sector austerity—to pay the banks’ bondholders. I am not sure who owns the bulk of Irish bank bonds, but there’s no reason to think it’s (i) bankers or even (ii) rich people (who, at least here in the U.S., tend to have barbell portfolios of tax-exempt bonds and equities),”

The bulk owners of Irish bank bonds are large European banks, primarily in France and Germany. In turn, the ultimate bondholders are ultimately the upper and middle classes in those countries.

I guess the best summation would be: the Irish are giving up their pension funds so the Germans can keep theirs. I don’t think that’s going to last very long.

hix 12.02.10 at 5:46 am

What is it with this Germany obsession?

Chris E 12.02.10 at 11:18 am

“I guess the best summation would be: the Irish are giving up their pension funds so the Germans can keep theirs. I don’t think that’s going to last very long.”

There’s some kind of circularity to all this isn’t there – with the same Germans under the impression that they are paying out to the Irish.

dsquared 12.02.10 at 11:46 am

I’ve mentioned this before I think; the reason that people think that “German Banks” have huge exposure to “Ireland” is related to the head office exposure of Hypo Real Estate AG to its subsidiary Depfa Bank plc. Depfa Bank plc (formerly DePfa AG, formerly Deutsche Pfandbriefanstalt, formerly Pruessische Landespfandbriefanstalt) is not an Irish bank in any economic sense of the word, and I think everyone reading this can guess why it shifted its headquarters to Dublin.

roger 12.02.10 at 12:55 pm

24. Yes, there is a lot of circularity here – as the same banks that the governments prop up trade the bonds that force the governments into ‘austerity’ measures. This is, to say the least, the sign of an inefficient market. Time, I would think, to simply call a halt to the present system of bond sales, create an international EU bond bank, and slice the head of the snake – to quote a Saudi king. It is as if the state – the ventriloquist – were being taken over by his dummy – the bank – from whom he is getting ‘loans’ to, well, prop up the bank.

An excellent thing for the dummy. But quite comic from any other standpoint.

Henry 12.02.10 at 3:35 pm

bq. I’ve mentioned this before I think; the reason that people think that “German Banks†have huge exposure to “Ireland†is related to the head office exposure of Hypo Real Estate AG to its subsidiary Depfa Bank plc. Depfa Bank plc (formerly DePfa AG, formerly Deutsche Pfandbriefanstalt, formerly Pruessische Landespfandbriefanstalt) is not an Irish bank in any economic sense of the word, and I think everyone reading this can guess why it shifted its headquarters to Dublin.

Is that all of the story? I did some reading around this issue a few days ago, and the “Bank for International Settlements”:http://www.bis.org/publ/qtrpdf/r_qt1009.pdf seems to be suggesting that German institutions are into Ireland for somewhere around the tune of 200 billion dollars (table on p.16). The estimates I’ve seen for Hypo Real Estate’s exposure (now apparently transferred to the German government’s bad bank) are for a little over 10 billion euro. This latter figure seems to have been leaked from the EU stress tests (I wasn’t able to find the original figures in the publicly released version of the stress test report, but various newspapers have been publishing that figure). I realize that contests taking the form of “bloke with Google” vs. “someone whose livelihood is built around their expertise” are usually not resolved in favor of the former, but if there is something odd or misleading-to-the-quick-once-over about the BIS figures, I would genuinely like to know, since I am writing a couple of pieces that use ’em.

ajay 12.02.10 at 3:46 pm

Henry: that HRE exposure figure is for Irish sovereign debt only, I think, as of the stress tests in the summer. The BIS figures are for exposure to Irish sovereign debt plus Irish bank debt plus other Irish debt, as of the end of Q1 this year (so even more out of date). Sorry if I’m pointing out the obvious here.

dsquared 12.02.10 at 3:52 pm

There is. Basically they’re not usable when one of the sides is a tax haven. HRE had 10bn-and-odd of direct exposure to the Irish government, per the CEBS test, but the issue is that although Depfa is a German bank for all economic and sensible purposes (and so wasn’t included in the stress tests), it’s an Irish bank for legal and regulatory purposes (and so it’s included as Irish exposure in the BIS statistics), so the whole intragroup exposure of HRE to Depfa gets recorded; the fact that it isn’t clean of head office effects is the main significance of the phrase “immediate borrower basis” in the footnote to that table. There are also all sorts of you-dont-have-to-be-Irish-to-be-Irish exposures relating to lending to insurance companies, lots of whom have a Dublin subsidiary, and even some ETFs are structured as Dublin SICAVs.

The problem is that there isn’t a better set of statistics than the BIS ones. Kieran’s mates Pierre Gourinchas and Helene Rey know their way around the BIS numbers like a black cab knows Mayfair, so they might have some ideas of how you get to the real exposure, but as far as I know, you basically can’t.

Henry 12.02.10 at 3:56 pm

Ah, all is explained.

dsquared 12.02.10 at 3:58 pm

(by way of reality check, total Irish sovereign debt outstanding is quite a lot less than $200bn, while the total balance sheet footings of AIB and BoI are of the order $200bn each. There just isn’t enough Ireland for Germany to have $200bn economic exposure to it).

bob mcmanus 12.02.10 at 4:00 pm

20: Everybody knows. The woman in the street doesn’t need to be told that finance is to blame.

She needs to shown that Revolution is possible and good. I think the whole problem is that a century of compromised liberals have told her the opposite.

The whole problem. The threat of guillotines has always been necessary.

Alex 12.02.10 at 4:05 pm

Bob: think, briefly, about the modern history of Ireland. Are you really in any place to recommend political violence to the Irish?

Pete Bogs 12.02.10 at 4:11 pm

I can’t stand seeing Eire in this state. We should all go visit and spend lots of money. First round is on me.

Chris E 12.02.10 at 4:28 pm

“by way of reality check, total Irish sovereign debt outstanding is quite a lot less than $200bn, while the total balance sheet footings of AIB and BoI are of the order $200bn each”

With the Irish state guarentee doesn’t this division get a lot more murky?

roger 12.02.10 at 4:29 pm

This site contains a useful BIS table on the nationality of banks exposed in various eurozone doa cases:

http://irelandafternama.wordpress.com/2010/11/24/the-web-of-european-bank-exposure/

bob mcmanus 12.02.10 at 5:16 pm

33: I am not recommending anything to Ireland (Latvia, Greece, USA) except perhaps Jubilee. And there are, by my definition, many stages and styles of Revolution short of “political violence.” (Unless you want to get into Weber/Schmitt/Agamben analysis)

Bob’s Rules for Revolutionaries:There is Only One Rule

The Ruling Class writes the Rules (ruling ideas, morals) in order to Rule.

It’s ok to break their rules.

Is that two? No, the first is analysis. Bob’s Rules covers everything from refusing to vote in a rigged election to default and mailing in your keys to storming the Winter Palace.

Oh. And as far as I am concerned, as just a guy in the street (in bankruptcy, with a family job outsourced to India, with insufficient healthcare) even the Radicals like Proyect and Seymour are just trying to lay more rules on me with their graduate level Trotskyism or whatever. Just safety valves for the Hegemony.

bob mcmanus 12.02.10 at 5:51 pm

It is probably linked in the OP, but here’s DeLong quoting Eichengreen on Ireland.

DeLong says Barry has gotten “very shrill.” But it is all description, all analysis, no prescription. What to do, what to do. Guess the Irish are just so screwed.

We need people like Eichengreen and Halasz to get just a little prescriptive, with any barest real possibility of a decent outcome. And no, electing a socialist legislature next century is not a responsible prescription.

Jubilee or burn shit down? But that will entail advocating breaking somebody’s rules. It will require courage, taking the point.

George J. Georganas 12.03.10 at 6:16 am

It is a mystery how some people can be liquidationist in one continent and can-kickers in another. If Irish banks had to be left to fail, why was letting Lehman fold wrong ? Does anyone now think TARP was wrong ? Banking is nothing more complicated than kicking the can down the road for ever and ever. Real trouble starts, once one begins to try to look virtuous by picking the can up and putting it in the rubbish bin. Deleveraging, purge the rotteness out of the system and the like. Essentially, liquidationists want the EU to do a CeauÅŸescu. Unvirtuous nations should not borrow, ever, goes the tune. A very sorry sight.

dsquared 12.03.10 at 9:05 am

… and just to show that these things happen in the best-ordered of families, today’s FT contains a story based on the BIS statistics which takes wrongness to a level not seen since … well, actually, since last quarter when the last set of BIS statistics came out. I note with a gulp that I first started saying that the BIS could do more to educate users in the correct use and limitations of the lending and exposure data in 1996!

ejh 12.03.10 at 12:32 pm

Bob: think, briefly, about the modern history of Ireland. Are you really in any place to recommend political violence to the Irish?

There might however be a very good case for recommending making-Ireland-ungovernable to the Irish, since it’s hard to see what, short of that, will prevent this appalling act of larceny and impoverishment being forced on them.

piglet 12.03.10 at 8:11 pm

“… and just to show that these things happen in the best-ordered of families, today’s FT contains a story based on the BIS statistics which takes wrongness to a level not seen since …”

Not everybody reads the FT, do you care to explain yourself?

enzo 12.04.10 at 2:03 am

Why is it Portugal-Spain-Italy… ? Surely the UK’s finances are worse than Italy’s: the deficit is double the size, for one thing. The speculators are partly political actors: they push countries in their preferred (neoliberal) direction. Ultimately the financial elite’s aim is to eradicate social democracy altogether, starting from the weakest links in the European chain. The UK is horribly complicit in this with its pandering to the bankers’ every whim — but that point leads to the whole USA-UK relationship can of worms, which may well be too far from what this post was about.

George J. Georganas 12.04.10 at 6:02 am

It is quite pointless to blame the bankers. It is the owners of savings that are in a state of panic now, not their agents any more. Whoc an blame the banker when homes go unsold for 11,700 euros ?

See this link http://www.bbc.co.uk/news/uk-northern-ireland-11835825

The question is whether it is good public policy to take control of those savings, for the good of their owners of course, in the hope that this panic will some day subside.

hix 12.04.10 at 11:25 am

Overall, real estate prices in Ireland, Spain and Uk are still far above German levels. Dramatic headlines about 11,700 houses that turn out to be about the first round of a forced sale for an unfinished appartment block dont change that.

George J. Georganas 12.05.10 at 6:42 pm

What about real estate prices in the USA ? Still too high, but no problem propping them up there. Why not in Europe ? I am sure , there are asset bubbles in many emerging markets. Why not advocate immediate liquidation of all risk assets, just to show who is really, really virtuous and perfectly conservative and prudent ?

In fact one can argue real estate prices in Germany have been kept artificially low by policy, not by the market, forcing German banks to place their excess funds into financing real estate in the US and losing a bundle in the process.

Robert Browne 12.06.10 at 5:07 pm

“The suddenness of the Irish deal has taken public opinion by surprise, causing shock that we have been plunged into this regime of austerity”

Not really. Below is what I said back in January on Michael Smiths’s blog but it was inevitable since Sept 08. For a synopsis read the fourth paragraph. What has happened is that the country has been betrayed by those too afraid to give up unjust salaries. They wanted to preserve their power, influence and money at all costs. What is going to happen next? Don’t want to frighten people!

Robert Browne Says:

January 23, 2009 at 4:18 pm

Brian Cowen and a bunch of “social partners†run the country. That is what he believes. Ergo, he believes in consensus, consultation, in groveling, in inertia he also believes in the innate kindness and reasonableness of the Social Partners. I don’t remember voting for social partners and I certainly don’t remember Mr. David Begg on any ballot paper!

Cowen seems genuinely afraid to lead. I ask myself, why on earth did he ever crave for this leadership job? Why did Mary Harney crave and demand the department of health? There is an inertia about him and this government that is bringing this whole country to its knees. That might not be as bad for us as we think. Of course, as a country we will resemble the third world first and it will be very painful. However, if you visit some of our hospitals, schools, abandoned housing estates or look at the dilapidated Roscommon Court House you might be forgiven for thinking you were already living in a third world country. Inside the court the blame game was in full flight, I digress!

Of course Cowen was a useless minister for finance just like McCreevy and Bertie before him. They squandered the ill gotten gains of the Celtic Tiger. Cowen would never cut a tax if he thought it was still generating a single euro for the exchequer. What was the logic of increasing VAT by a half a percent to twenty one and a half per cent? Just to be sure to be sure that people would go to the north to shop! Scrooge school of economics is what I call it. Trying to explain to him that raising taxes blunted consumer confidence, would lead to hoarding of cash, would lead to jobs being shed at accelerating rates would mean rising unemployment and longer dole queues was like trying to explain the theory of quantum physics to an infant.

The only luminosity on the horizon is that when this government cannot meet Anglo’s debts, cannot cover BOI and AIB’s debts and cannot repay sovereign debt, it will have no choice, but to allow the ECB and IMF in to call the shots. This will happen sooner rather than later because of the damage Ireland is doing to the reputation of the Euro and Eurozone.

I firmly believe, when they come in, that, we will begin to have a proper HSE for half the fourteen billion it currently costs us. We will have investment in rat infested and leaking primary schools, cheaper power when the “private†ESB and An Bord Gais are again brought under the proper remit of those vested with running the state. These two energy entities have been hi-jacked by their members and are being run like private fiefdoms. When oil was one hundred and forty seven dollars a barrel they were shouting it from the roof tops as they proceeded to crucify people with insane energy bills. It seems the equation does not work the other way around! That is, when oil falls your gravity defying energy bill stays at the ludicrous level it was inflated to.

The way the country has been milked of taxpayers funds, the shameless way our politicians have wasted the money, the fact that no one resigns, and no one goes to jail informs us clearly of the sorry state our democracy is in ninty years after the first Dail. The last thing our “patriots†in Dail Eireann want is to face the dole queues themselves, this means, that the whole squalid performance will carry on until foreigners come in and run the country for us!

Comments on this entry are closed.