The most recent data from Eurostat bring out starkly the implications of the current policy mix in the Eurozone. The peripheral economies continue to be spun around by an inflexible centre, and whether they fly off in a crisis remains anyone’s guess.

On the face of it, as the following graph suggests, some economies are easily diagnosed as having fiscal deficit problems. It is not hard to see how German public opinion can be persuaded that fiscal profligacy is the problem and that a dose of austerity will bring them back into line with German fiscal virtue.

Italy and Belgium actually have larger accumulated debts than Portugal or Spain, but they have no immediate problems keeping their debts rolling over. Britain falls into the same cluster with its combined debt and deficit problems, but no-one is seriously worried about its policy options.

Italy and Belgium actually have larger accumulated debts than Portugal or Spain, but they have no immediate problems keeping their debts rolling over. Britain falls into the same cluster with its combined debt and deficit problems, but no-one is seriously worried about its policy options.

The peripheral economies have problems that are different in kind, different from Germany and also from each other.

Greece, which entered the crisis with a poorly functioning public sector, has to try to achieve major and painful institutional surgery in the direct of circumstances.

Meanwhile, Ireland’s quite staggering 32% deficit in 2010 is mostly attributable to the enormous expense of what the Governor of the Central Bank has called ‘one of the costliest bank crises in history’. Minister for Finance Michael Noonan noted that the state will be committing 45% of GDP to the banks over a two-year period – which Mohamed El-Erian of PIMCO has called ‘a debacle’ and which Nouriel Roubini warned would ‘break the government’s back’. Spain has a similarly distressed if not quite so catastrophic financial sector. Portugal has long struggle with problems of sluggish growth.

There are two major problems with the course of action required of the European periphery, especially now that Greece and Ireland are both in an EU-IMF-ECB loan programme and Portugal is about to enter one.

The first is that fiscal austerity will do nothing at all to address the banking crisis. Bad domestic policy caused the crisis in Irish and Spanish banks, but there is no scope for domestic crisis resolution policy through restructuring the liabilities. Instead, EU and ECB policy requires the entire burden of adjustment be taken into the sovereign debt. But there are serious sustainability as well as equity problems with this.

The second is while that the whole point of fiscal austerity is to create the conditions under which growth can resume so the bond markets will recover confidence in these countries’ capacity to service their borrowings, this policy is proving to have serious perverse consequences.

European policy interventions, consistently characterized as too little and too late, have failed to reverse pessimistic market assessments.

Poor growth continues to characterize the European periphery, because these countries are locked into measures that further depress economic activity (GNP is normally reported for Ireland too because of the significance of the FDI sector in GDP):

The peripheral economies have already taken a very bruising spell of adjustment. Ireland, for example, is still a wealthy country in comparative terms, but relatively speaking it has taken a bigger hit than others (and GNP is about one-fifth lower than GDP):

The peripheral economies have already taken a very bruising spell of adjustment. Ireland, for example, is still a wealthy country in comparative terms, but relatively speaking it has taken a bigger hit than others (and GNP is about one-fifth lower than GDP):

Real GDP and GNP in Ireland are estimated to be down about 15% from the peak point, and nominal GDP and GNP are down by about 24%. The internal distribution of pain is also uneven. Unemployment, a little over 4% in 2006, is now 14.7%, ripping out from the collapse in construction into other sectors. For those in employment, incomes have taken hit after hit with across-the-board headline reductions in nominal pay in the public sector, repeat increases in taxation and other charges, and cuts in spending on transfers and services.

Real GDP and GNP in Ireland are estimated to be down about 15% from the peak point, and nominal GDP and GNP are down by about 24%. The internal distribution of pain is also uneven. Unemployment, a little over 4% in 2006, is now 14.7%, ripping out from the collapse in construction into other sectors. For those in employment, incomes have taken hit after hit with across-the-board headline reductions in nominal pay in the public sector, repeat increases in taxation and other charges, and cuts in spending on transfers and services.

Time and again we have seen that as soon as one of the peripheral countries engages in serious austerity measures, the ratings agencies downgrade their government bonds.

Speculation appears to be increasing now that Greece will simply be unable to continue on its current path, notwithstanding a variety of harsh measures already taken and more to come. Next in line are Ireland and Portugal, though Spain is not under serious pressure at this point. The markets clearly don’t accept the assumption that these countries will be able to exit their life-support measures and borrow openly again as projected for sometime in 2012 or 2013:

Economist Colm McCarthy is calling this a ‘slow-motion train-wreck’.

Economist Colm McCarthy is calling this a ‘slow-motion train-wreck’.

{ 9 comments }

Chaz 05.03.11 at 9:33 am

That last chart is incredibly confusing. I would recommend plotting them all relative to the bund (and the bund not at all) or all relative to 0%.

Nice post, otherwise. If Ireland’s GDP has been overstated by 20% this whole time, people should point that out a lot more often.

Cahal 05.03.11 at 10:06 am

This is a joke. The credit rating agencies/banking cartel need to be neutralised or this kind of crap will just continue.

Random lurker 05.03.11 at 1:52 pm

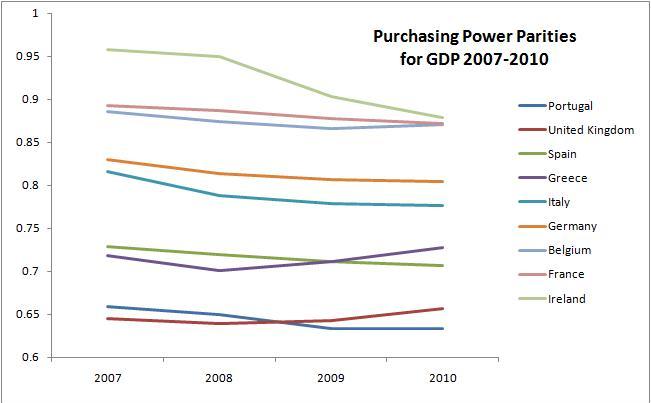

The third graph seems to show that in purchasing-power-parity terms Greece and the UK are better off now than at the beginning of the crisis.

Is this real? This would surprise me.

Billikin 05.03.11 at 2:38 pm

About the first graph: “On the face of it, as the following graph suggests, some economies are easily diagnosed as having fiscal deficit problems.”

I do not understand the diagnosis. Every country seems to have deficit problems, in that as they have reduced their deficits, their debt has grown. (Of course, these are ratios to GDP. Perhaps we can say that every country has a GDP problem?) Greece has the worst slope, but why? Germany’s slope is worse than Ireland’s or Spain’s. Should that concern the Germans? I am afraid that I do not see what conclusions to draw from this graph.

niamh 05.03.11 at 9:34 pm

@ Billikin, the point of the graph is to illustrate the current debate in Europe about how best to deal with problem economies. The peripheral economies have a heavy combined debt and deficit load at the moment and this makes them an easy target for those who would press for fiscal austerity as a cure-all. But this wont’ work. The point is developed below the fold.

@Random Lurker, I haven’t gone back to check the precise OECD data definitions, but for relative ‘wealth’ PPP is probably a better measure than simple GDP per capita, or price indicators. If GDP has fallen but prices have fallen even further in enforced internal competitiveness, surely these trends would be expected.

@ Chaz, I could’ve reported the figures in tabular form as they appear in the Eurointelligence post linked in the text, but I thought the picture looked nice. The triumph of aesthetics over – oh no! – over intelligibility, not so good…

John Quiggin 05.04.11 at 3:45 am

Thanks for this useful post. It’s unfortunate in lots of ways that Greece was the first to require a bailout. Everything since has been fitted into a framework of profligacy vs austerity. While I would argue that Ireland should have run larger surpluses before the crisis and dampened down the boom, the real disaster was the decision to guarantee the banks, and the loss there would have overwhelmed even the most fiscally prudent of governments.

John Quiggin 05.04.11 at 3:50 am

A minor point is that the shift from reporting GNP (normal in the 1960s) to GDP is highly problematic, unless you are doing short-term macro analysis. The best general purpose measure, and the best for assessing financial sustainability, is actually Net National Income.

Andrew Latimer 05.04.11 at 11:23 pm

I like the change in GDP chart — to me the surprising part of this is the high UK apparent growth in 2010. Reflects later onset of austerity budgeting there than Greece, Ireland, Spain?

Enda H 05.06.11 at 1:53 am

Hi Niamh,

Time and again we have seen that as soon as one of the peripheral countries engages in serious austerity measures, the ratings agencies downgrade their government bonds.

You seem to be suggesting a causal link here. Is that intentional?

Comments on this entry are closed.