One Spring Monday in 1852 around thirty gold buyers gathered for the evening at Mrs Black’s Royal Hotel in Bathurst, which was (and is) just on the other side of the Blue Mountains from Sydney.

Probably not ordinarily the most collegiate of petty capitalists, the gold buyers gathered to debate the role of the local branch of the Union Bank of Australia in undercutting their business.

The bank had begin purchasing gold at a slightly higher rate than individual gold buyers could do, bringing diggers in from the gold fields to Bathurst where they would get a better deal – and (so rejoiced the local storekeepers) use some of their earnings to buy some Fancy Goods.

Some gold buyers thought this was fair of the bank, which added gentlemanly respectability to what was recently a frontier townships.

Others noticed that the bank was cutting out the middleman. And since they were the middlemen, that was pretty uncool.

Mr Samuel, certainly one or the other of the Messrs L & S Samuel, gold buyers of Bathurst, reminded those gathered that gold was not actually money. Banks have no more business trading in gold, he told his comrades, than they had trading in wool, tallow or sheepskins (which tells you what other business was in in Bathurst in those days).

Image: Australian Joint Stock Bank Gulgong, Holtermann Collection SLNSW. Coloured by AI.

Gold buyers came in many shapes and sizes. Some were buyers only, many were metallurgists who assayed the gold as well. We know about them because they were sometimes called into court to act as witnesses. Their extensive experience with gold meant that they could identify where gold came from.

For example, Joseph Aarons (OK lets admit I start with him because he comes up in the As of gold buyers) was in court to identify a piece of gold that someone or other was accused of stealing and then selling onwards to a bank – such accusations were really common. It seems that banks were not always all that fussed about how gold had been acquired. Their job was just to buy it. In fact, a story from Gulgong’s Pioneer Museum, which I visited last weekend, told of the police entering the Australian Joint Stock Bank to chase down a gold thief. The bank manager not only refused to allow the police officer to search behind the bar (Ok I know that’s not what it is called in a bank, but surely in this case…), but they also pulled out a pistol, prepared to take action to prevent the police search.

Anyway, Joseph Aarons, clearly a more upstanding fella than he Gulgong bank manager, testified in court about the gold under question. I’ve bought SO MUCH gold he said. And this gold is definitely from Wentworth.

Nathan Wilson, a jeweller from Sydney, also said. Yeeah, I’ve bought gold from Wentworth before too. It isn’t great gold, I didn’t like it. This gold is just like that.

Aside – did you know there were differences in gold like this? Not me!

So a whole lot of these gold experts are running around buying gold. It is transported (under guard…more about this in the future) to the Treasury in Sydney, which we know because they published long lists of gold buyers and quantities of gold they received from each.

From this (and also advertising by gold buyers in the newspapers) we know that lots of gold buyers were women.

Not all gold buyers were all that expert. Some were just buying and selling gold alongside their other buying and selling of stuff.

Richard Binnie was one of these. He left school at 14 like most other people and began an apprenticeship that he pursued for a year before realising he had an entrepreneurial itch. His diaries tell us about the contracts he had with government stores in New South Wales and Melbourne to supply goods. In his 30s, Binnie went on a whirlwind trip to San Fransisco in 1850 where he was very impressed with the stores selling neatly packaged goods that were easy for diggers to purchase and transport. He made a long list of goods that could be sent from New South Wales, and what prices they would fetch in California. He later audited the local Australian Joint Stock Bank where, amongst all the cash, he found $11,733 worth of gold dust. Richard Binnie just bought gold sometimes as part of his diverse set of business activities.

Money brokers were part of this world of folk finance. Before the gold rushes, banks in Australia didn’t normally deal with small stuff. They didn’t really do small loans so people couldn’t borrow what they needed for their quartz-crushing gold extracting start up, to buy their beloved a carving knife (one of the things on Binnie’s list of things to buy for his ‘Lizzie’) or even to purchase property. Banks were there mainly to discount bills of exchange, which made them a pretty minor industry on the edge of international shipping rather than the utility that they later became.

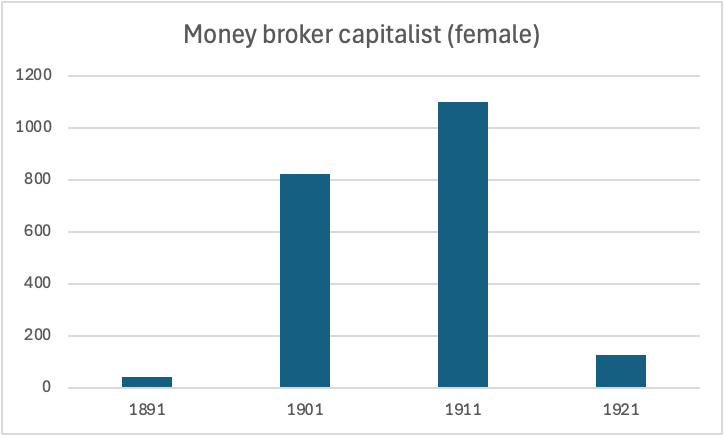

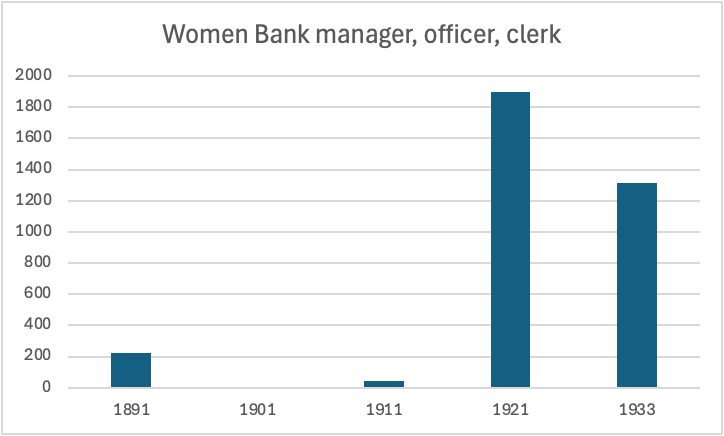

So money brokers were where people went when they needed a loan. Like lots of businesses that one could do on one’s own account, by the 1890s when demand for small amounts of credit grew to significant proportions, lots of these money brokers were women. Now the 1890s was not a great time for banks (in fact, lots of them crashed in that decade). But we can see from the graph that by the 1910s, money broking is not really a thing. Fortunately (or something) the Great War was about to break out, so that the very rapidly growing occupation of bank clerks would soon experience a man shortage, opening up many opportunities for young women to enter banking. But that is another story.

Data source: Australian and Australian colonial censuses

Data source: Australian and Australian colonial censuses

The system also cracked down on the gold buyers. Endless rumours of dodgy deals between gold buyers and folk sneaking into mines in Bendigo to snaffle the gold encouraged the Bendigo newspaper to advocate for registration and regulation of Gold Buyers.I haven’t yet read the 1901 gold buyers act, but I did read the 1907 one that replaced it. It required Gold Buyers to only purchase gold from a clearly marked place of business. And insisted that gold sellers must walk through the front door, in daylight hours.

But by then the issue that the gold buyers raised in Mrs Black’s Royal Hotel in Bathurst in 1852 was pretty much resolved in favour of the banks. Sure, banks were not likely to deal much in tallow or sheepskins, but gold was definitely their business. So too were loans, for that matter. Much easier to regulate, to be sure. But it also meant that the generations of women (and men) who profited by making money from money were now more likely to work as a bank clerk in exchange for wages.

It amounts to a kind of industrialisation of finance work. By 1919, bank workers in Sydney formed a union. Working conditions in banks were bleak enough that union membership grew at a rate of around 50-60 members a day just in Sydney.

But that too is another story.

This post is part of my Fellowship at the State Library of NSW. The project is entitled ‘what happened to the gold?’

{ 1 comment }

D. S. Battistoli 06.25.26 at 8:18 am

Thank you for such a delightful article!

You write:

Now, what I am about to say starts with context, and moves toward

In the contemporary global south, it is not uncommon for mining multinationals, often Australian and Canadian, to work in the same country as so-called “artisanal” gold miners (who are also heavily mechanized in most cases). Now the difference between the seams exploited by the multinationals and the “artisans” basically comes down to the following: it is possible to turn a profit in extracting, refining, and trading (or extracting and trading to a refinery operation) gold in what we can call the multinational seams when all activities are performed at their price points. Artisanal seams need to operate at a discount, which is produced by having them exploited by largely informal outfits who are then bargained down on price. (And of course, around the world, different seams are of different quality, leading to different, localized but globally determined price spreads if artisanal miners are involved).

In the end, all gold is turned either into jewelry-quality or bullion and, incidentally, is thence very untraceable to its source. In domestic markets like the one here in Senegal, where gold is mined but not refined, there are two market prices: domestic gold (artisinally mined in West Africa; industrially mined gold doesn’t re-enter the global market except as part of a finished prodict) and “Swiss gold” (the metal refined to one or another international standard, after having been mined by multinationals or artisans).

Now, I am curious, based on your post: as you look at the turn-of-the-century gold value chain in Australia, do you see a similar multi-track value chain developing, with one side formally controlled by capitalists from the mine to final production, and another with significant parts outsourced to less-formal groups, whose products tended to get “bid down” at the point where they entered a heavily capitalized operation?

Comments on this entry are closed.